Tariffs Cannot Be All Things To All People

Arguing

for tariffs in 2024 because Alexander Hamilton favored them is like

saying we should bring back bloodletting because it was used on George

Washington.

It is alarming to watch the leading candidates for Treasury Secretary in the second Trump administration compete over who can do the best impression of Smoot and Hawley, the most infamous protectionists in American history. Perhaps aware that the economic argument for tariffs is weak, the two reported top contenders to steward America's economy have resorted to misguided appeals to history. Howard Lutnick of Cantor Fitzgerald, leader of the president-elect's transition team, said that America was last great during the McKinley administration, when high tariffs were the primary source of federal revenue. Not to be outdone, Scott Bessent of Key Square Capital Management went even further back in history, extolling Hamiltonian tariff policies from the republic's earliest days.

Arguing for tariffs in 2024 because Alexander Hamilton favored them is like saying we should bring back bloodletting because it was used on George Washington. America today is not an agricultural economy struggling to emerge from the economic shadow of a former imperial overlord. Nor does the nation have a 19th-century government on the gold standard and small enough to be financed mainly through tariffs—unless the new administration plans to eliminate Medicare, Social Security, the Pentagon, and more.

The incoming administration's approach to tariffs is deeply conflicted. While paying rhetorical homage to President-elect Trump's love of universal tariffs, Mr. Bessent also argues for the "strategic" use of tariffs as leverage. Mr. Lutnick has previously said tariffs can be a "bargaining chip." Yet officials from the Trump transition are reportedly talking to Congress about legislating across-the-board universal tariffs of 10-20% (and 60% on China) as part of next year’s tax bill. This idea may be attractive to some on Capitol Hill because tariffs can be "scored" as helping to offset the budgetary cost of renewing or expanding the 2017 Tax Cuts and Jobs Act. But this would mean the tariffs -- and the revenue they are expected to produce -- are intended not to be transitory bargaining chips but permanent fixtures of federal fiscal policy.

Tariffs cannot be all things to all people, and the new administration will soon need to clarify its tariff strategy.

Our trading partners know that a tariff baked into a large tax bill and scored by the Congressional Budget Office as a "pay-for" cannot be easily traded away. Doing so would require another act of Congress, and finding alternative revenue sources to replace the tariffs. Other countries will not bargain with the United States over market access if they suspect that America cannot deliver the removal of legislated tariffs.

Tariffs imposed via executive action are not as immutable as legislation but can still be quite “sticky.” Take, for example, the U.S. tariff on light trucks. Following a trade dispute in 1964 with Europe over the poultry trade, the Lyndon Johnson Administration imposed a retaliatory 25% tariff on pickup trucks as reciprocal leverage to resolve the dispute. The "chicken wars" with Europe ended long ago, but the pickup tariff remains today. If you've ever wondered why America's most popular vehicle costs an average of $60,000, look to the stickiness of “reciprocal” truck tariffs imposed in a long-ago fight over chicken.

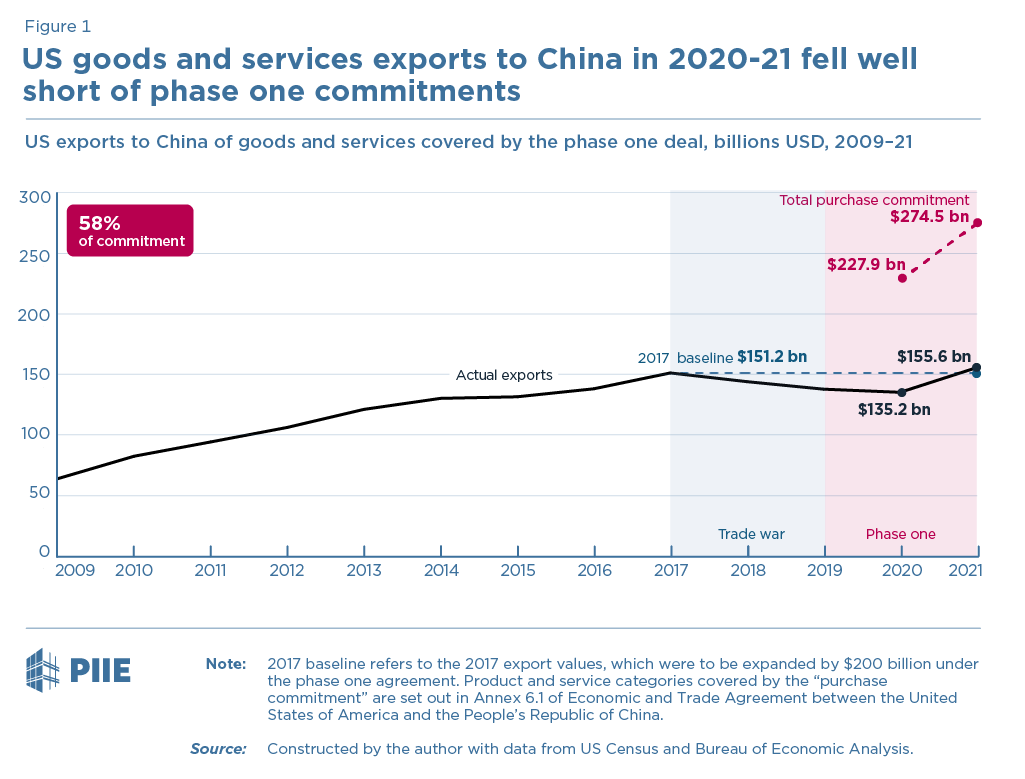

A more recent example is President-elect Trump's first-term tariffs on China, which were intended to force China into making large-scale purchases of American exports. But the "Phase One" deal reached with China in 2020 did not produce what was promised; according to a 2022 analysis by Chad Bown of the Peterson Institute for International Economics, "China bought only 58 percent of the US exports it had committed to purchase under the agreement, which was not even enough to reach its import levels from before the trade war." (See chart below).

Manufactured exports to China, especially autos and aircraft, were hit hard by the trade war and did not fully recover. The trade deficit with China was reduced, but the overall U.S. trade deficit increased (significantly) during President Trump's first term; most of the reduction in the bilateral deficit with China came from production being shifted to other Asian countries, not relocated to the United States.

The first-term Trump tariffs on China affected approximately $380 billion of trade. They failed to deliver market access in China, hurt the U.S. economy, cost jobs, and increased prices for consumers. Now, the president-elect vows to raise tariffs on $3.8 trillion of trade, ten times more than his first foray into "strategic" protectionism. America will be lucky if the results are only ten times worse.